Web3 protocols - Faster growth, less funding, and quicker exits that Web2 companies

Venture-backed Web3 protocols scale faster than their Web2 counterparts

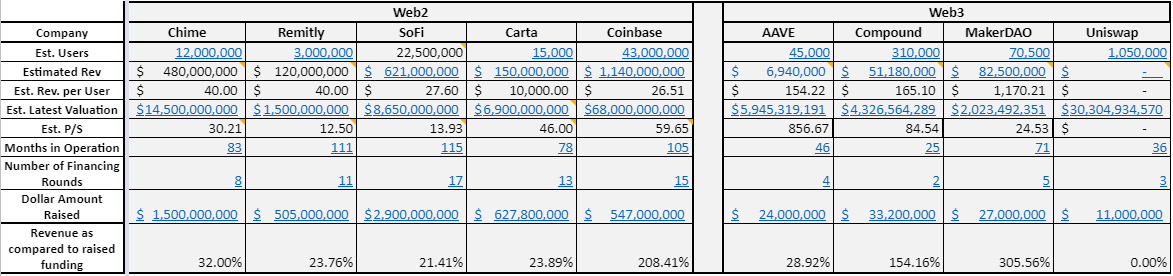

An analysis of Web2 companies and Web3 protocols shows that the latter grew faster in terms of valuation and revenue per venture dollar raised. The results, as shown below, were clear; Web3 protocols grew faster and in some cases larger, despite being younger and armed with less financing. On top of this, the investments in Web3 protocols are already partly, if not entirely, liquid -- all in a matter of 3 years on average. This stands in stark contrast to the Web2 companies in the analysis who, despite being on average 8 years old, all remain private.

For this analysis we took the latest (2020 to-date) implied or stated revenue run rates for each of the Web2 companies based on their respective latest equity financings and compared it to the revenue run rates of Web3 protocols using on-chain annualized data from the past 30 days. We then took this revenue comparison and visualized it against the total amount of money raised to-date for each company.

Though other fundamental and relative valuation arguments can be drawn from this analysis (of which we may do in another post in the future), it is important to remember the key question that spawned this research effort....

Do Web3 protocols grow faster than their Web2 counterparts?

Analysis Overview:

Summary comparison measuring total Web3 revenue

Summary comparison measuring Web3 protocol revenue only

FYI, the analysis file is linked here - please see embedded comments for assumptions & explanations. Feel free to reach out if you have any questions and/or comments.

Key Highlights:

Web2 metrics (5 companies):

$6.09B - Money raised over the lifetime of the companies

$2.511B - Estimated sum of all latest revenue rates (calculated using latest implied revenue run rates ~ 1yr)

Average company age 96 months (8.2 years)

Total aggregate market capitalization = $100 Billion (2/3 ‘s of which is attributable to Coinbase)

Web3 metrics (4 protocols):

$95.2M - Money raised over the lifetime of the companies

All revenue (30-day period annualized) - $1.77B

Protocol-only revenue (30-day period annualized) - $140.6M

Average company age 36 months (3.08 years)

Total aggregate market capitalization = $48 Billion

-The five Web2 companies in the analysis posted combined latest revenue rates of ~42% of the money they raised in aggregate.

-The four Web3 protocols in the analysis posted combined annualized revenue rates of nearly 150% of the money they raised in aggregate (protocol only revenue). This number grows to 1860% or 18.6X when swapping for the all revenue view.

-Discounting Coinbase, the aggregate market capitalizations of the Web2 companies is ~30% less than the aggregate of the Web3 protocols'.

Side-by-Side Comparison

Uniswap:

On a “total revenue” basis, Uniswap’s latest annualized revenue run rate nearly matches that of Coinbases’, despite Coinbase raising 50X more funding and being 3X older.

On the same basis, the differences between Carta and Uniswap are even more stark. Uniswap, at half the age of Carta, has an annualized revenue run rate 7.5X higher than Carta’s despite raising only ~1.5% of the money.

All revenue (LP revenue + Protocol revenue)

Protocol revenue only

Compound:

Compound has generated more revenue than money raised at just over two years old --- no matter which revenue view you take.

On an all revenue basis, Compound’s latest annualized revenue run rate is nearly ⅔’s that of SoFi - a company that has plans to go public in 2021. On the same basis, Compound nearly matches Chime’s latest revenue run rate despite being much younger and raising ~2% of the money Chime did.

Even on a protocol only revenue basis, Compound’s revenue per dollar raised is far better than Chime’s and SoFi’s.

All revenue (Supply-Side revenue + Protocol revenue)

Protocol revenue only

Aave:

No matter which view you take, Aave has more revenue per dollar raised than Chime and SoFi.

All revenue (Supply-Side revenue + Protocol revenue)

Protocol revenue only

---

MakerDAO:

No matter which view you take, MakerDAO has more revenue per dollar raised than Chime and SoFi.

All revenue

Protocol revenue only (NO DIFFERENCE)

Deeper Analysis

- Why Did this Happen?

- Implications & What comes next - VC's & Investment liquidity

Why did this happen? - Every company in this analysis has done very well, but were Web3 primitives the catalysts? We think so. Examples:

Aligned Incentives - Users who drive value to a protocol becoming part owners in that protocol and the existence of broader aligned economic incentives between a network and its users have created a new form of network effects that allows protocols to attract and retain high value users. In a domain where growth begets more growth, this tight loop between users and protocol/value ownership has created a native flywheel that drives growth and distribution.

Verifiable & instant metrics - Many Web3 protocols build in the open. What that means is that for many, their user count, revenues & other financial/growth metrics are published to the blockchain and thus able to be queried/verified at any time. This ability has led to faster feedback loops and shorter reaction times between product teams, their users, and markets. Put plainly, for Web3 protocols building in the open, the world can know and financially respond to growth, contraction, and other important business updates much faster than in traditional finance. Since people are more likely to adopt a product if their growth statistics are already large, this native Web3 capability has helped power explosive growth.

Token utility - Protocol-native assets/currencies that could be used for *something* else in DeFi wound up driving adoption. Whether it was yield farming, staking incentives, or another primitive - the more a holder could do with the protocol token, the more that user interacted with the system and drove value.

Implications & What comes next - VC's & Investment liquidity:

---VC's

Depending on the relationship of the protocol to its original development company post-decentralization, protocol companies may not ever have to raise external money after they've decentralized and distributed control and ownership of the protocol. For example, it would make sense that Uniswap and Compound raised financing rounds prior to their distribution events, but post-distribution, there's a high likelihood that the protocol's governance-controlled treasury is sitting on hundreds of millions, if not billions, of dollars of assets that could be used to fund growth in lieu of outside investment. Being that most token distribution events have been at Series A or prior (with dYdX as an exception), this could mean that early-stage Web3 VC’s will have an entirely new focus and heightened importance level moving forward as the source of Web3 growth-stage funding shifts.

I say "depending on the relationship between the protocol to its development company..." above because while it may be clear that the protocol may not need to raise any additional outside funding, the original development company (which post-decentralization would be two distinct things) may have to. The % of the distribution retained, if any, by the development company + the protocol's rules/willingness about governance-granted funding back to the original development team will likely help determine that outcome in practice. In the future, it will be interesting to see what Uniswap Labs and Compound Labs do in this area given their structure and funding parallels to this narrative.

Capital will need to be bonded together with the type of hard technical/economic specializations and skills that are proven to increase the chances of a project's success. Examples of proprietary tooling:

Community building

Fair launch mechanisms

Airdrop targeting tools & methodologies

Sustainable incentives and rewards schemas for users to become owners in the protocol(s) they drive value to

Governance minimization tactics

KPI-driven airdrop/option designs (See UMA's latest example here)

Exit-to-community best practices

Legal advice for everything above

---Investment liquidity

Stakeholders in Web3 protocol companies may continue to see faster liquidity events in the form of governance token and/or network-native currency launches -- possibly in addition to equity in the parent company they've invested in depending on deal/company structure.

If the above is accurate, quicker liquidity events could shorten the cycle time of successful founders and early employees exiting a successful company and investing the profits in the next generation of companies in the domain - creating even more capital availability and intense investor competition.

Conclusion:

Web3 protocols have far more native corporate transparency, investment liquidity, price discovery, more efficient rails as compared to fiat, and offer ownership tied with usage. This makes it hard to compare their metrics to Web2 company metrics fairly.

Both VC’s and founders should be attracted to the liquidity, network effects, rapid growth, and stickiness that potentially comes with the development and use of Web3 primitives.

Protocols do not work for every type of business or venture, nor should they be the sole focus of a VC as opposed to traditional equity, but at this point in their adoption cycle ignoring their existence will only grow more costly.

Web2 companies did not grow as fast as Web3 protocols, but were up against different rules at the time and in some still are. Many Web3 protocols grew organically, in an open setting, and without similar hurdles. For example: KYC, Apple/Google app store arbitrary rules, and various other jurisdiction-based regulations likely took and continue to take Web2 companies time, effort, and focus to comply with. This route the Web2 companies took, in turn, gave them access and proximity to the legacy operating and financial systems that would-be users operate in (iOS, ACH). This is NOT to give an opinion that Web3 protocols were/are not compliant in any way (that's not for me to say), but still is worth pointing out.

Disclaimers:

This analysis is not intended to be a knock on the Web2 companies in question, all of which are great companies with fantastic products and employees. It is simply an illustrative effort to show the differences between two sets of successful company structures.

If you have any questions, comments, and/or concerns about the information above please do not hesitate to reach out.

The contents above are for illustrative and informational purposes only.

The contents above are not to be used, in any way, as legal, technical, financial, and/or professional advice. Please do your own research and consult your own appropriate parties/counsel prior to decision making.

The contents above are provided “as is” and without warrant/guarantee to their accuracy.

We reserve the right to amend any part of this post or data analyses linked/posted within.

Nothing above or posted within is a recommendation and/or solicitation to buy securities.

Comments

Post a Comment